Younger Canadians drive 125% surge in cashback rewards

Chexy, the Canadian fintech platform that enables consumers and businesses to earn credit card rewards on recurring payments like rent and bills. It is becoming a key tool for younger Canadians cashback rewards. New data shows cashback card usage through the platform is increasing 2.5 times faster among users under 40 than those aged 40+. Cashback transaction volume among users under 40 rose 125 per cent between Q4 2025 and Q1 2026.

Based on an analysis of overall Chexy user activity, cashback transactions rose 97% over the same period, while users earning cashback grew 60%. This signals both rapid adoption and increased usage frequency among existing users. This momentum reflects a broader repositioning of rewards from passive perks to active financial strategy, led by younger Canadians, who are shifting to cashback at 2.5 times the rate of those 40 and over.

The generational divide is also evident in how value is distributed across the platform. Canadians under 40 processed $24.7 million in cashback volume in Q1 2026 compared to $11.6 million among those 40 and over. Younger users drive this gap. They now make up the majority of the platform’s user base. When controlling for headcount, older users actually transact more per person. This highlights two distinct behaviours. One focused on maximizing value in real time. The other is rooted in larger, more consistent individual spending patterns.

“Rewards are no longer something Canadians earn passively over time, they’re becoming an active part of how spending is managed day to day,” said Liza Akhvledziani, Founder and CEO of Chexy. “Younger Canadians are leading this shift. They’re prioritizing flexibility and immediacy, using cashback as a way to unlock value in real time on the expenses they already have, rather than waiting to accumulate rewards over the long term.”

Why cashback is rising amid cost-of-living pressure

The timing of this shift is notable. Cost-of-living pressures remain elevated and household budgets tighten. The expectation that spending should deliver immediate, tangible value is becoming more pronounced. Cashback aligns with that mindset, it offers a form of liquidity. Many Canadians are looking for ways to make their money go further without changing how or where they spend.

At the same time, the data suggests this is not purely reactive behaviour. The scale and speed of growth point to broader evolution in financial habits. This is especially true among younger consumers. They have come of age in an environment shaped by real-time payments, flexible financial tools and on-demand services. For this group, rewards are no longer a passive benefit. Rather, they are an active part of how spending is managed.

Together, the data points to a broader shift. Rewards are becoming less about long-term accumulation alone, and more about how value can be accessed, used, and adapted in the moment.

QUICK FACTS

How is Chexy expanding beyond rent payments?

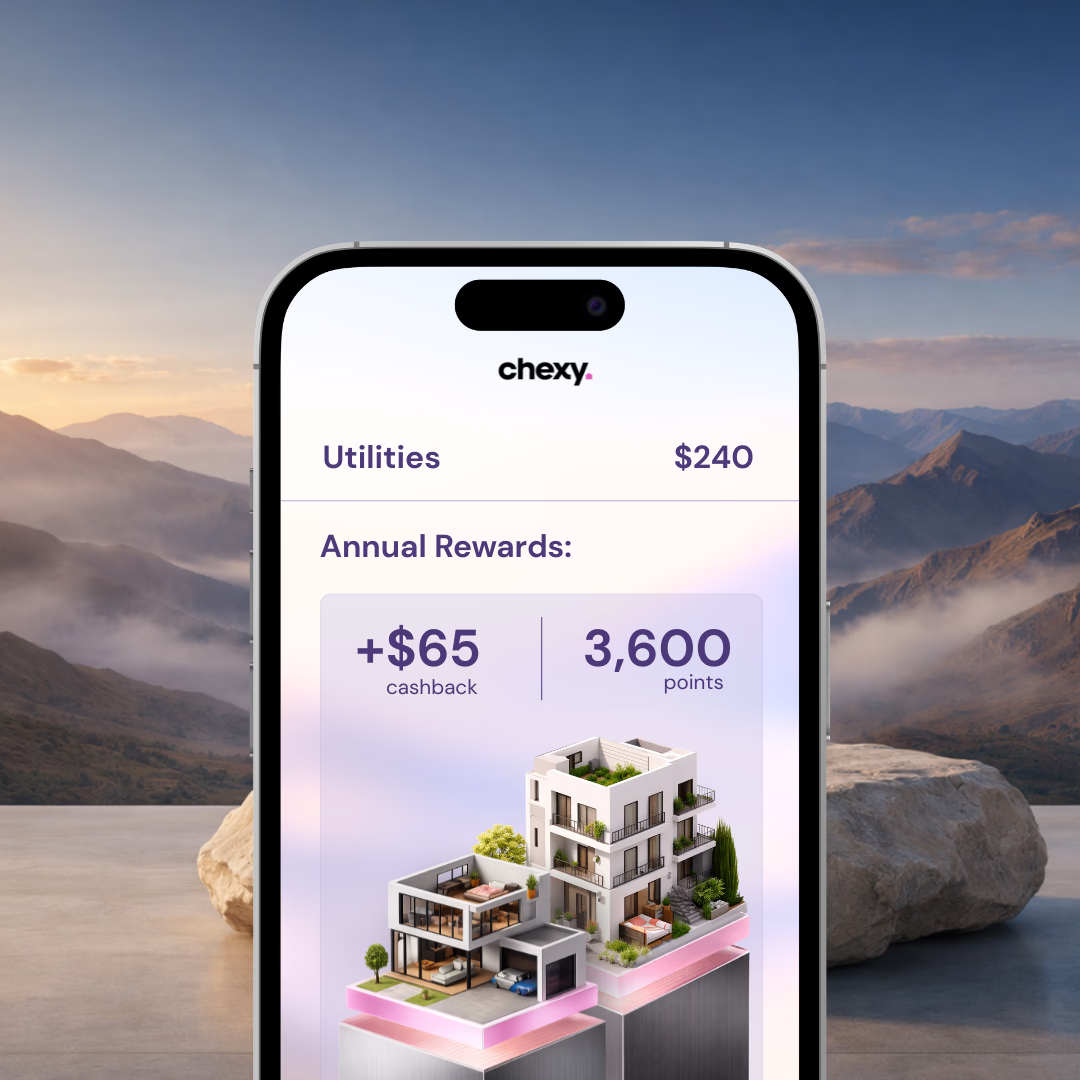

Chexy now supports a wider range of recurring payments, including utilities, taxes, and vendor payments, helping consumers and businesses earn rewards where credit cards were traditionally not accepted.

How many users does Chexy have?

Chexy serves more than 200,000 users across Canada.

How do Aeroplan rewards integrate with Chexy?

Chexy users can earn Aeroplan points on recurring payments such as rent, taxes, and bills through the company’s partnership with Aeroplan.

Why are Canadians earning rewards on everyday expenses?

Major household expenses like rent, utilities, and taxes make up a large share of spending, yet historically have not earned rewards.

Which credit cards work best with Chexy?

Chexy works with all major Canadian credit cards, with the most value often coming from travel rewards and cashback cards.

What unexpected use case is emerging for Chexy?

Chexy is seeing growing use among SMBs paying vendors, taxes, and payroll, as well as increased interest from landlords and property managers seeking more modern, rewards-driven payment experiences.

For more on how data is reshaping financial behaviour in Canada, see our work with Sapling Financial Consultants here.